The cost of drugs for age-related macular degeneration in Canada and internationally

PDF - 821 kb

Age-related macular degeneration (AMD) is the leading cause of irreversible blindness in Canada, affecting approximately 2 million CanadiansFootnote 1. New anti-vascular endothelial growth factor (anti-VEGF) drugs have been launched to treat the neovascular (wet) form of AMD, along with a number of other retinal conditions. While anti-VEGFs have improved therapy outcomes for these conditions, they come with a high price tag. By 2017, sales of these drugs accounted for 2.8% of the total Canadian pharmaceutical market. This analysis provides insight into the sales, uptake and prices of this class of drugs in Canada and internationally.

These findings will form the basis for a more comprehensive study on anti-VEGF drugs to be published as part of the PMPRB Market Intelligence Report series. This series provides detailed information on specific therapeutic market segments of importance to Canadians to inform policy discussions and aid in evidence-based decision making.

The analysis focuses on ranibizumab (Lucentis), which was approved for market in Canada in 2007, and aflibercept (Eylea), which was introduced in 2013. The international markets examined include the seven countries the PMPRB considers in reviewing the prices of patented drugs (PMPRB7): France, Germany, Italy, Sweden, Switzerland, the United Kingdom (UK) and the United States (US); as well as other countries in the Organisation for Economic Co-operation and Development (OECD).

1. Anti-VEGFs used to treat retinal conditions have seen rapid sales growth over the past decade

In 2007, Lucentis became the first anti-VEGF launched in Canada approved for wet AMD as well as other important retinal diseases. It was quickly recognized as the new gold standard for treatment. In 2013, Eylea was also approved for AMD and launched at a slightly lower price; other indications were later added.

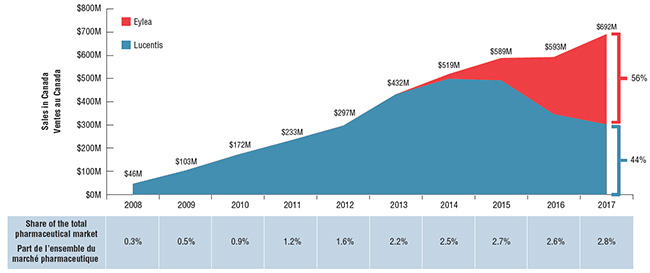

Combined sales for these two drugs reached $692M in 2017. Until 2013, in the absence of a competitor, Lucentis had dominated the market and enjoyed solid growth; however, by 2017 Eylea had surpassed it in annual sales. In 2017, Eylea captured 56% of the combined sales, reflecting a slightly greater share of actual units sold (59%) due to its lower cost.

Trends in Canadian sales for Lucentis and Eylea, 2008-2017

Click on image for larger view

Figure description

This area graph shows total annual combined sales for Lucentis and Eylea in Canada from 2008 to 2017. In 2017, Eylea accounted for 56% of combined sales, while Lucentis was 44%. Sales values are expressed in millions of dollars. The table below the graph shows the combined sales as a percentage of the total Canadian pharmaceutical market share.

blank

| Year |

Lucentis |

Eylea |

Total |

| 2008 |

$46 |

$0 |

$46 |

| 2009 |

$103 |

$0 |

$103 |

| 2010 |

$172 |

$0 |

$172 |

| 2011 |

$233 |

$0 |

$233 |

| 2012 |

$297 |

$0 |

$297 |

| 2013 |

$432 |

$0 |

$432 |

| 2014 |

$499 |

$20 |

$519 |

| 2015 |

$492 |

$97 |

$589 |

| 2016 |

$346 |

$247 |

$593 |

| 2017 |

$302 |

$389 |

$692 |

blank

| Year |

Total Canadian pharmaceutical market share |

| 2008 |

0.30% |

| 2009 |

0.50% |

| 2010 |

0.90% |

| 2011 |

1.20% |

| 2012 |

1.60% |

| 2013 |

2.20% |

| 2014 |

2.50% |

| 2015 |

2.70% |

| 2016 |

2.60% |

| 2017 |

2.80% |

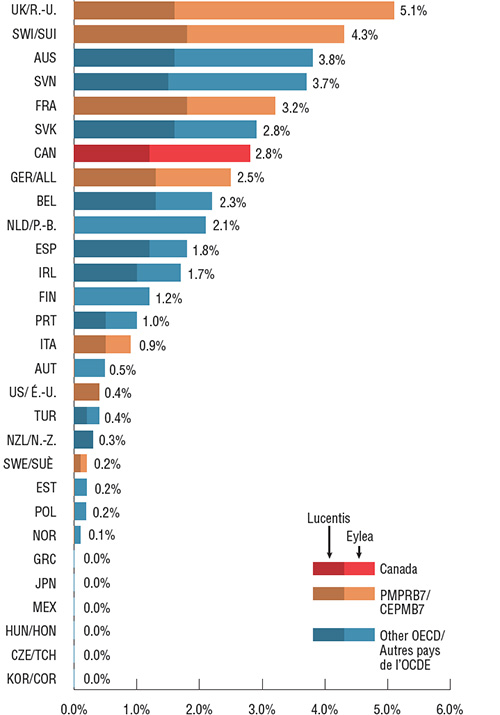

2. Lucentis and Eylea account for a higher pharmaceutical market share in Canada than in most other OECD countries

Lucentis and Eylea accounted for 2.8% of total pharmaceutical sales in Canada in 2017, the seventh-highest share in the OECD. Of the PMPRB7 countries, Canada placed fourth behind the UK, Switzerland, and France. In general, a higher comparative market share may point towards a higher rate of consumption, higher prices, or a combination of both factors, although it is also affected by the relative sales in the rest of the pharmaceutical market.

Eylea had higher sales than Lucentis in 17 of the 29 OECD countries with available data, similar to the distribution in Canada. In the top 10 countries with the highest combined market share, Eylea captured at least 40% of sales. Notably, Eylea had less than 0.1% of the total pharmaceutical market share in the US, the lowest of all PMPRB7 countries.

Share of total pharmaceutical sales for Lucentis and Eylea, OECD countries, 2017

Click on image for larger view

Figure description

This bar graph shows the 2017 combined market share of Lucentis and Eylea sales in Canada, the seven PMPRB comparator countries countries, and other Organisation for Economic Co-operation and Development countries. The sales mix of Lucentis and Eylea is also displayed for each country.

blank

| Country |

Lucentis |

Eylea |

Total |

| United Kingdom |

1.6% |

3.5% |

5.1% |

| Switzerland |

1.8% |

2.5% |

4.3% |

| Australia |

1.6% |

2.2% |

3.8% |

| Slovenia |

1.5% |

2.2% |

3.7% |

| France |

1.8% |

1.4% |

3.2% |

| Slovakia |

1.6% |

1.3% |

2.8% |

| Canada |

1.2% |

1.6% |

2.8% |

| Germany |

1.3% |

1.2% |

2.5% |

| Belgium |

1.3% |

0.9% |

2.3% |

| Netherlands |

0.0% |

2.1% |

2.1% |

| Spain |

1.2% |

0.6% |

1.8% |

| Ireland |

1.0% |

0.7% |

1.7% |

| Finland |

0.0% |

1.2% |

1.2% |

| Portugal |

0.5% |

0.5% |

1.0% |

| Italy |

0.5% |

0.4% |

0.9% |

| Austria |

0.0% |

0.4% |

0.5% |

| United States |

0.4% |

0.0% |

0.4% |

| Turkey |

0.2% |

0.2% |

0.4% |

| New Zealand |

0.3% |

0.0% |

0.3% |

| Sweden |

0.1% |

0.1% |

0.2% |

| Estonia |

0.0% |

0.2% |

0.2% |

| Poland |

0.0% |

0.1% |

0.2% |

| Norway |

0.0% |

0.1% |

0.1% |

| Greece |

0.0% |

0.0% |

0.0% |

| Japan |

0.0% |

0.0% |

0.0% |

| Mexico |

0.0% |

0.0% |

0.0% |

| Hungary |

0.0% |

0.0% |

0.0% |

| Czech Republic |

0.0% |

0.0% |

0.0% |

| South Korea |

0.0% |

0.0% |

0.0% |

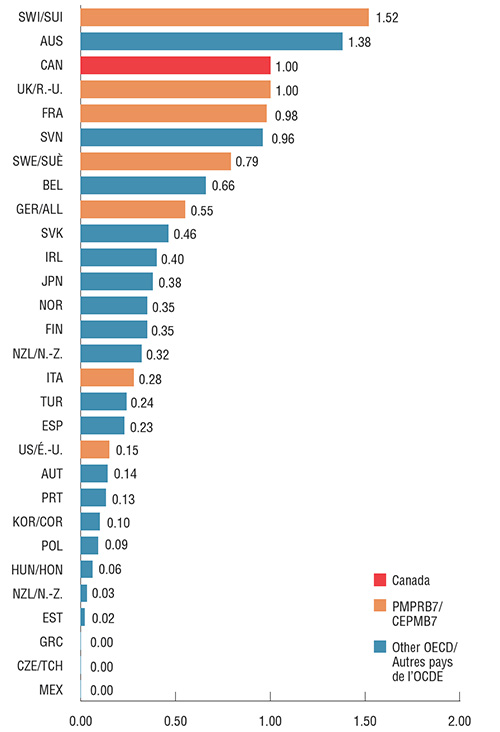

3. Consumption of Lucentis and Eylea in Canada is among the highest in the OECD

Canada has the third highest per capita consumption of Lucentis and Eylea in the OECD. The findings are presented as an index, where the consumption rate in Canada is set to 1 and the rates in other countries are reported relative to this value.

In the PMPRB7, only Switzerland has a higher rate of consumption. Like Switzerland, Australia, the UK and France, Canada has both a high consumption rate and a high combined share of total pharmaceutical sales, indicating that the Canadian experience with Lucentis and Eylea is similar to that in other developed countries. Low consumption in the US and other markets may be due, in part, to the off-label use of Avastin for retinal conditions, which due to data limitations is not considered in this analysis.

Annual combined Lucentis and Eylea consumption rate* indexed to Canada, OECD countries, 2017

Click on image for larger view

*Based on the PMPRB Human Drug Advisory Panel (HDAP) annual maintenance treatment dose per patient. Assumed 0.5 mg dose for Lucentis and 2 mg dose (0.05 ml) for Eylea, regardless of standard volume listed for each country in MIDAS™.

Figure description

This bar graph compares 2017 combined Lucentis and Eylea consumption per million inhabitants in the seven PMPRB comparator countries and other Organisation for Economic Co-operation and Development countries. The results are indexed to Canadian consumption, which is set at 1.00.

blank

| Country |

Total annual dose ratio |

| Mexico |

0.00 |

| Czech Republic |

0.00 |

| Greece |

0.00 |

| Estonia |

0.02 |

| New Zealand |

0.03 |

| Hungary |

0.06 |

| Poland |

0.09 |

| South Korea |

0.10 |

| Portugal |

0.13 |

| Austria |

0.14 |

| United States |

0.15 |

| Spain |

0.23 |

| Turkey |

0.24 |

| Italy |

0.28 |

| Netherlands |

0.32 |

| Finland |

0.35 |

| Norway |

0.35 |

| Japan |

0.38 |

| Ireland |

0.40 |

| Slovakia |

0.46 |

| Germany |

0.55 |

| Belgium |

0.66 |

| Sweden |

0.79 |

| Slovenia |

0.96 |

| France |

0.98 |

| United Kingdom |

1.00 |

| Canada |

1.00 |

| Australia |

1.38 |

| Switzerland |

1.52 |

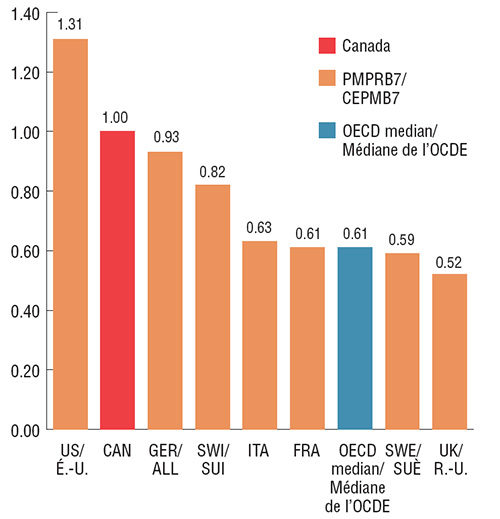

4. Canadian prices for Lucentis and Eylea are at the higher end of the OECD spectrum

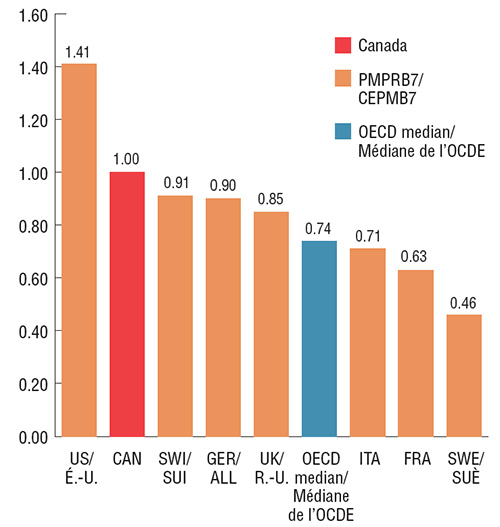

In the last quarter of 2017, Canadian prices for Lucentis and Eylea were second only to the US among the PMPRB7 comparator countries, and significantly higher than the OECD median. The median PMPRB7 price for Lucentis, set by Italy, was 37% less than the Canadian price; while the PMPRB7 median for Eylea was the 15% less, set by the UK. These results indicate the potential for significant cost implications if Canadian prices were closer to median international levels.

Foreign-to-Canadian price ratios for Lucentis, Q4-2017

Click on image for larger view

Figure description

These two side-by-side bar graphs give the foreign-to-Canadian price ratios for Lucentis and Eylea in the fourth quarter of 2017. Results are given for each of the seven PMPRB comparator countries as well as the median value for the Organisation for Economic Co-operation and Development countries.

Lucentis

| Country |

Foreign-to-Canadian price ratio |

| United Kingdom |

0.52 |

| Sweden |

0.59 |

| OECD median |

0.61 |

| France |

0.61 |

| Italy |

0.63 |

| Switzerland |

0.82 |

| Germany |

0.93 |

| Canada |

1.00 |

| United States |

1.31 |

Foreign-to-Canadian price ratios for Eylea, Q4-2017

Click on image for larger view

Figure description

Eylea

| Country |

Foreign-to-Canadian price ratio |

| Sweden |

0.46 |

| France |

0.63 |

| Italy |

0.71 |

| OECD median |

0.74 |

| United Kingdom |

0.85 |

| Germany |

0.90 |

| Switzerland |

0.91 |

| Canada |

1.00 |

| United States |

1.41 |

5. Higher prices for Lucentis and Eylea translated into approximately $168 million for Canadian payers in 2017

The price differentials between Canadian and foreign markets translate into substantial cost implications for Canada. If Canadian prices for anti-VEGFs were aligned with the PMPRB7 median price levels for the fourth quarter (Q4) of 2017, the national Canadian sales for Lucentis would have been up to $110.4M (36.5%) lower in 2017, while sales for Eylea would have been $57.9M (14.9%) less. Similarly, the cost implications for public plans would have been $79.7M for Lucentis and $26.5M for Eylea for the 2016/17 fiscal year.

Cost implications of higher Canadian prices for Lucentis and Eylea using the Q4-2017 PMPRB7 median price

| |

National Market (all payers), 2017 |

Canadian public drug plans, 2016/17 |

| BC |

AB |

SK |

MB |

ON |

NB |

NS |

PE |

NL |

YK |

NIHB |

Total

public |

| Lucentis |

Total drug cost |

$302.3M |

ND |

$11.1M |

$2.2M |

ND |

$195.7M |

$4.1M |

ND |

$0.2M |

$2.4M |

<$0.1M |

$2.6M |

$218.3M |

Cost implications

(share of total cost) |

$110.4M

(0.45%) |

ND |

$4.1M

(0.55%) |

$0.8M

(0.24%) |

ND |

$71.5M

(1.55%) |

$1.5M

(0.79%) |

ND |

$0.1M

(0.21%) |

$0.9M

(0.75%) |

<$0.1M

(<0.01%) |

$1.0M

(0.21%) |

$79.7M

(0.99%) |

| Eylea |

Total drug cost |

$389.4M |

NL |

ND |

$3.1M |

NL |

$170.3M |

$3.1M |

NL |

$0.4M |

$0.3M |

<$0.1M |

$0.6M |

$177.8M |

Cost implications

(share of total cost) |

$57.9M

(0.24%) |

NL |

ND |

$0.5M

(0.41%) |

NL |

$25.3M

(0.55%) |

$0.5M

(0.25%) |

NL |

$0.1M

(0.19%) |

<$0.1M

(0.04%) |

<$0.1M

(<0.01%) |

$0.1M

(0.02%) |

$26.5M

(0.33%) |

ND: product is reimbursed, but no data is available. This may be due to reimbursement through a special eye care plan.

NL: product is not reimbursed.

Note: Bevacizumab (Avastin), which was launched in 2005 and is used off-label as an intravitreal therapy for some retinal conditions, was not considered in this analysis. Health Canada and other international regulatory bodies including the EMA and FDA have only approved Avastin for use in the treatment of certain types of cancers. Although it is prescribed off-label for retinal conditions, the data does not differentiate between indications and thus it was not included in the study. The extent of its use varies widely by jurisdiction.

Limitations: Canadian and international sales and list prices available in the IQVIA MIDAS™ database are estimated manufacturer factory-gate list prices and do not reflect off-invoice price rebates and allowances, managed entry agreements, or patient access schemes.

Sources: Availability, uptake and pricing information in this analysis were determined based on the IQVIA MIDAS™ database (all rights reserved); public drug plans costs were obtained from NPDUIS, Canadian Institute for Health Information.

Disclaimer: Although based in part on data provided under license by the IQVIA MIDAS™ Database, the statements, findings, conclusions, views and opinions expressed in this report are exclusively those of the PMPRB and are not attributable to IQVIA.

NPDUIS is a research initiative that operates independently of the regulatory activities of the PMPRB.